Financial Equity in Couples – For generations, the financial advice given to couples moving in together, getting married, or combining their lives has been startlingly simple: split everything right down the middle. The “50/50” rule is deeply ingrained in our culture. It feels mathematically perfect, wonderfully clean, and entirely objective. After all, if two people are sharing a life, a home, and a future, shouldn’t they share the costs equally?

On paper, it makes sense. In reality, treating a romantic partnership like a collegiate roommate agreement is a recipe for long-term resentment. When two modern adults merge their lives, they rarely bring identical salaries, identical debts, or identical capacities for household management. Applying a rigid framework of equality (equal dollars) to an inherently unequal reality destroys equity (fairness based on circumstance and capacity).

To build a sustainable, friction-free relationship, couples must move beyond the illusion of equal financial contributions and build a system rooted in true, holistic equity. Here is how to make the shift from a stressful 50/50 split to a balanced, proportional partnership.

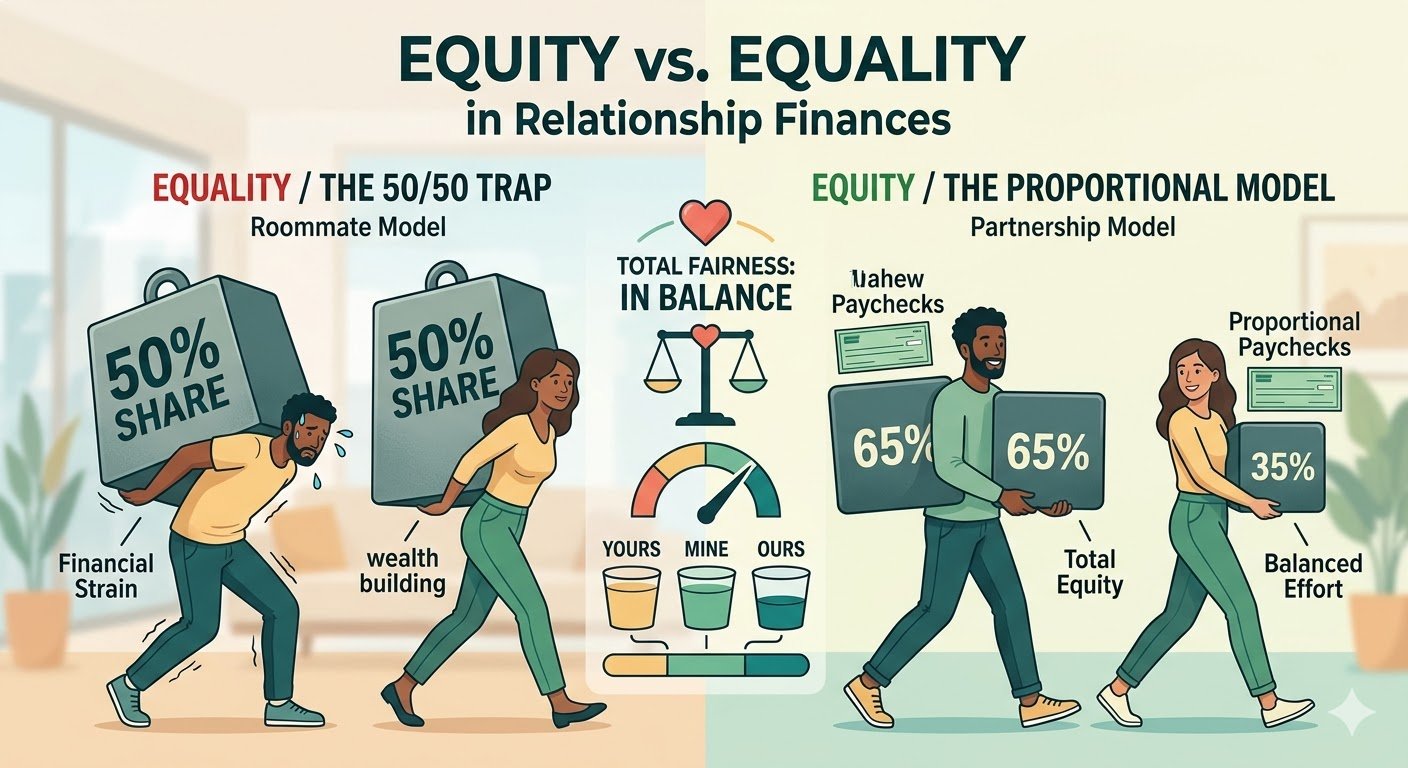

1. The Danger of “Equality” (The 50/50 Trap) (Financial Equity in Couples )

The fundamental flaw of the 50/50 split is that it assumes both partners experience the exact same economic reality. It ignores the context of their individual paychecks. When there is a significant income disparity within a relationship, a strict equal-dollar split creates immediate, systemic stress for the lower earner.

The Math of Financial Suffocation

Let’s look at the mathematics of a standard modern household. Imagine a couple whose shared living expenses—rent or mortgage, groceries, utilities, and shared insurance—total $4,000 a month.

Under a strict 50/50 split, each partner is required to contribute $2,000.

- For Partner A (Earning $100,000/year): Their monthly take-home pay is roughly $6,000. That $2,000 contribution accounts for just 33% of their income. After the bills are paid, Partner A is left with $4,000 of surplus cash for personal savings, investments, and guilt-free hobbies.

- For Partner B (Earning $50,000/year): Their monthly take-home pay is roughly $3,000. That identical $2,000 contribution consumes a staggering 66% of their entire income. After covering their own individual costs—like student loans or a car payment—Partner B is left financially suffocating, living paycheck to paycheck.

The Parent-Child Power Dynamic

This mathematical disparity quickly erodes the emotional foundation of the relationship. Because the lower earner is stretched so thin, they lose their financial autonomy. If the couple wants to take a vacation, go out for a celebratory dinner, or even buy a nice piece of furniture for the apartment, Partner A has to “treat” Partner B.

What started as an “equal” split morphs into a toxic Parent-Child dynamic. The higher earner begins to feel like a benefactor or an ATM, while the lower earner feels like a dependent who must ask for permission to participate in their own life. This loss of adult agency is the leading cause of financial infidelity, where partners begin hiding small purchases simply to reclaim a sense of control.

2. Defining True Equity: The Proportional Model

Financial equity is not about everyone paying the exact same dollar amount; it is about everyone feeling the exact same relative level of financial “pinch.” The healthiest, longest-lasting relationships utilize an Income-Proportional Split.

In an equitable system, both partners contribute a percentage of the household expenses that directly mirrors their percentage of the total household income. It shifts the burden from equal dollars to equal effort.

How to Calculate the “Equal Pinch”

Setting up a proportional split requires radical transparency, but the math is straightforward:

- Find Your Total “Us” Income: Add your monthly take-home pay together. If Partner A brings home $6,000 and Partner B brings home $3,000, your total household income is $9,000.

- Determine Your Contribution Ratios: Divide your individual income by the household total.

- Partner A: $6,000 / $9,000 = 66.6%

- Partner B: $3,000 / $9,000 = 33.3%

- Fund the Family Ledger: For your $4,000 in shared monthly expenses, Partner A contributes 66.6% ($2,664), and Partner B contributes 33.3% ($1,336).

This structure ensures that the financial weight of the shared life is carried collaboratively. Most importantly, it leaves both partners with a proportional, fair amount of “Mine” money. This is personal capital they can spend with complete autonomy, free from guilt, judgment, or “input interrogation” from their partner.

3. The Missing Currency: Validating the “Mental Load”

A proportional financial split beautifully solves the bank account problem, but it does not solve the entire equity equation. A relationship does not run on dollars alone; it runs on three distinct currencies: money, time, and cognitive energy.

If a couple perfectly balances their financial contributions, but the lower-earning partner is still expected to act as the default “Household Manager,” the relationship remains deeply inequitable. This invisible labor—often called the Mental Load—is the grueling, behind-the-scenes work of anticipating needs, identifying solutions, and monitoring outcomes.

The Cost of Invisible Labor

The mental load is the background operating system of a shared life. It is the labor of:

- Noticing the dog is out of food, researching the best price, and ensuring it gets delivered on time.

- Auditing the pantry to build the weekly grocery list and meal plan.

- Tracking shared subscriptions to ensure the household isn’t overpaying.

- Remembering the in-laws’ birthdays and organizing the gifts.

If one partner provides a larger portion of the capital, but the other partner is managing the complex, exhausting logistics of the “Us” entity, their total contributions to the relationship are actually quite balanced. However, because society only measures value in dollars, the partner managing the mental load often feels unseen, exhausted, and undervalued.

True equity requires a system that tracks, validates, and celebrates this invisible labor right alongside the financial deposits. You must measure Total Contribution, not just financial contribution.

4. The Architecture of Transparency

To make this equitable system function without daily friction, couples must build the right banking architecture. You cannot run a proportional split while trying to Venmo each other back and forth for every single utility bill or grocery run.

Couples must adopt the “Yours, Mine, and Ours” framework:

- The “Ours” Account: A joint checking account specifically for the “Family Ledger.” Both partners automatically transfer their proportional percentages into this account every payday. All shared bills are paid from here.

- The “Mine” Accounts: Your individual checking accounts. The money left in these accounts after the proportional transfer is strictly yours. It represents your financial autonomy and should never be micromanaged by your partner.

5. Automating Equity with EvenUS

The theory of holistic financial equity is beautiful; the manual execution of it can be exhausting. Attempting to track fluctuating proportional splits, variable utility bills, and daily household chores on a shared Excel spreadsheet creates massive administrative friction.

Eventually, the friction of maintaining the spreadsheet outweighs the benefits of transparency. Couples get tired of doing the math, and they default back to the stressful 50/50 model or rely on one person to blindly pay for everything.

To make equity sustainable, you need an automated, neutral third party. That is exactly why we built EvenUS.

EvenUS is the relationship operating system designed to finally move modern couples beyond the 50/50 trap.

- Dynamic Proportional Splits: You simply input your incomes, and the app calculates exactly what is fair based on real-time data. If you get a raise or a bonus, the system updates your contributions automatically. No spreadsheets, no arguments over the math.

- Mental Load Validation: EvenUS is the first platform to track household “Zones,” chore management, and the invisible cognitive labor that keeps your life running. We take the invisible work and make it visible.

- The Total Fairness Score: By combining your financial input with your time and domestic effort, the app generates a single, objective metric. It visualizes your holistic contribution, proving that both partners are pulling their weight in their own unique, deeply valuable ways.

Stop letting outdated roommate advice dictate your modern romantic relationship. Equity is about building a system where both people feel seen, valued, and secure.

To validate the “Mental Load” and Invisible Labor

Source: American Sociological Review Study: The Cognitive Dimension of Household Labor (2019) Author: Allison Daminger (Harvard University) Why it fits your article: This study formally identifies and categorizes the four stages of the “Mental Load” (Anticipating, Identifying, Deciding, Monitoring). It provides sociological proof that cognitive labor is a distinct, exhausting form of work that is typically ignored when couples only look at financial contributions.