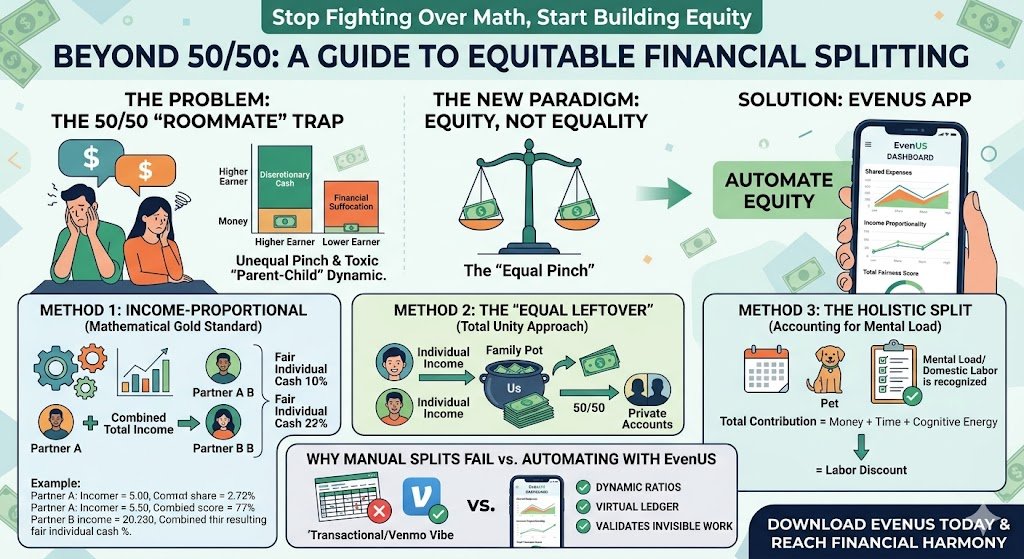

Calculating Fair Financial Splits – In the modern romantic landscape, the phrase “let’s split it” has become one of the most loaded sentences a couple can utter. For decades, the default setting for cohabiting couples—whether dating, engaged, or married—has been the “roommate model”: a rigid, 50/50 division of all shared expenses.

On the surface, 50/50 feels like the ultimate expression of equality. However, as contemporary sociological and economic research suggests, treating a partnership like a business merger between two equal-resource entities often leads to a systemic power imbalance. When incomes are unequal, an equal-dollar split creates a “Financial Suffocation” effect for the lower earner, while the higher earner builds wealth with disproportionate ease.

To protect the long-term health of a relationship, couples must transition from a mindset of equality (equal dollars) to a mindset of equity (fairness based on capacity). This article explores the mathematical frameworks, psychological research, and best practices for calculating fair financial splits that actually work.

The Psychology of the “Equal Pinch” (Calculating Fair Financial Splits )

The core philosophy behind equitable splitting is the “Equal Pinch.” This concept argues that the fairness of a financial contribution shouldn’t be measured by the absolute dollar amount, but by the impact that contribution has on the individual’s remaining quality of life.

According to research published in the Journal of Financial Therapy, financial arguments are rarely about the price of a specific item; they are about the loss of autonomy. When a lower-earning partner spends 60% of their take-home pay on “their half” of the rent while the higher-earning partner only spends 20%, a toxic “Parent-Child” dynamic emerges. The higher earner becomes the default “benefactor” who must pay for vacations or dinners, while the lower earner feels like a dependent.

To dismantle this, couples must choose a calculation method that balances the household ledger while preserving individual agency.

Method 1: The Income-Proportional Split (The Mathematical Gold Standard)

The Income-Proportional Split is the most widely recommended framework for modern, career-focused couples. It ensures that both partners contribute the exact same percentage of their income toward shared survival, leaving both with a fair, proportional amount of discretionary cash.

The Calculation Framework

- Calculate Combined Net Income: Add both partners’ monthly take-home pay (after taxes).

- Determine Individual Percentages: Divide each individual’s income by the combined total.

- Apply to the Shared Ledger: Multiply those percentages by the total cost of shared household expenses (rent, utilities, groceries, shared debt).

Real-World Example

- Partner A (Higher Earner): $6,500/mo (65% of total)

- Partner B (Lower Earner): $3,500/mo (35% of total)

- Total Household Income: $10,000/mo

- Total Shared Bills: $4,000/mo

The Math:

- Partner A pays 65% of $4,000 = $2,600

- Partner B pays 35% of $4,000 = $1,400

The Result: Both partners are contributing exactly 40% of their own paycheck to the household. Partner A is left with $3,900 of “Mine” money, and Partner B is left with $2,100. While the absolute dollar amounts differ, the “pinch” to their daily lifestyle is identical.

Method 2: The “Equal Leftover” Method (The Total Unity Approach)

For couples with extreme income gaps—or those who subscribe to a “What’s mine is ours” philosophy—the proportional split might still feel too individualistic. If one partner earns $150,000 and the other earns $40,000, even a proportional split leaves the higher earner with a massive surplus of wealth while the other stays relatively stagnant.

The “Equal Leftover” method prioritizes lifestyle parity over individual earnings.

The Calculation Framework

- Pool All Income: Treat both paychecks as a single “Family Pot.”

- Fund the Shared Ledger: Pay all household bills, shared savings, and joint investments from this pot.

- Divide the Remainder: The remaining surplus is divided 50/50 and transferred into individual accounts for personal spending.

Real-World Example

- Total Combined Income: $12,000

- Total Shared Expenses: $5,000

- Remaining Surplus: $7,000

The Result: Each partner receives $3,500 into their private “Mine” account. This method ensures that neither partner ever feels “poorer” than the other in their daily life, effectively removing income as a source of status within the marriage.

Method 3: The Holistic Split (Factoring in the Mental Load)

The most significant flaw in traditional financial advice is that it only measures capital. However, a household runs on three distinct currencies: Money, Time, and Cognitive Energy.

Research by Harvard sociologist Allison Daminger identifies the “Mental Load”—the invisible, exhausting labor of anticipating needs, identifying solutions, and monitoring household logistics—as a distinct form of work. In many relationships, the partner who earns less money compensates by managing 80-90% of the household logistics.

How to Calculate “Total Fairness”

If Partner A provides the majority of the capital, but Partner B acts as the “Household COO” (managing groceries, cleaning, pet care, and scheduling), a 50/50 or even a strict proportional financial split is actually unfair to Partner B.

The Best Practice: Couples should assign a “Labor Discount” or value to domestic management. For example, the couple may agree that because Partner B manages the entire domestic “Zone,” Partner A will cover 100% of the fixed mortgage and utilities, while Partner B only covers variable costs like groceries. This validates the time and energy Partner B invests, ensuring both partners feel their total contribution is seen.

The Execution Trap: Why Manual Splits Fail

Understanding the math is the easy part; executing it consistently is where most couples fail. Most people attempt to manage these splits via a shared spreadsheet or a monthly “settling up” conversation. This creates two major problems:

- Administrative Friction: Tracking every grocery receipt and utility fluctuation is tedious. Eventually, one partner stops logging, the data becomes inaccurate, and arguments ensue.

- The “Venmo Roommate” Vibe: Constantly requesting money from a spouse feels transactional rather than romantic. It keeps the relationship in a state of “Me vs. You” rather than “Us.”

Automating Equity with EvenUS

To make these research-backed frameworks sustainable, you need an automated, neutral third party. This is exactly why the EvenUS app was developed.

- Dynamic Ratios: EvenUS connects to your accounts and automatically calculates your income-proportional ratio in real-time. If you get a bonus or a raise, the math updates instantly—no calculators required.

- Virtual Joint Ledger: You can keep your separate bank accounts while using EvenUS as a “Virtual Joint Pot.” It tracks shared spending and tells you exactly how to stay balanced.

- Validating the Invisible Work: EvenUS is the first platform that allows you to log domestic labor and household management alongside financial contributions. It synthesizes all three currencies—money, time, and effort—into a single Total Fairness Score.

When a system handles the math and validates the effort, money stops being a source of conflict and starts being a tool for your shared future.

The psychological impact of financial disparity in relationships is well-documented. For a deeper dive into how income inequality affects relationship quality and the “Parent-Child” dynamic mentioned above, you can access the primary research here:

- Journal of Marriage and Family: The Division of Household Labor and Family Enjoyment

- American Sociological Review: Cognitive Labor: The Invisible Dimension of Domestic Work