When we hear the term “financial infidelity,” our minds usually jump to cinematic extremes: a secret second family, a hidden gambling addiction, or a drained life savings account.

But in reality, financial infidelity rarely starts with a massive betrayal. It usually starts in the trunk of a car. It starts with hiding a shopping bag before walking into the house, downplaying the cost of a new gadget, or quietly opening a private credit card just to have some “breathing room.”

These small omissions might feel like harmless white lies designed to keep the peace. In truth, they are the first cracks in the foundation of your relationship. Here is why we lie to our partners about money, the damage those small secrets cause, and how to build a system where you never have to hide a receipt again.

The Spectrum of Financial Infidelity in Relationships: From White Lies to Shadow Accounts

When financial advisors or relationship therapists talk about “financial infidelity,” most people immediately picture catastrophic scenarios. You imagine a spouse gambling away the kids’ college fund or siphoning money into a secret offshore account.

Because we picture these extreme cinematic betrayals, it is incredibly easy to justify our own minor deceptions. We tell ourselves, “I’m not committing financial infidelity; I just didn’t tell him how much I spent at Sephora.” But financial infidelity is simply any intentional deception regarding money within a committed relationship. It exists on a spectrum. It rarely starts with a massive betrayal; it usually begins with small, everyday omissions designed to “keep the peace.”

Here are the three most common stages on the spectrum of financial infidelity:

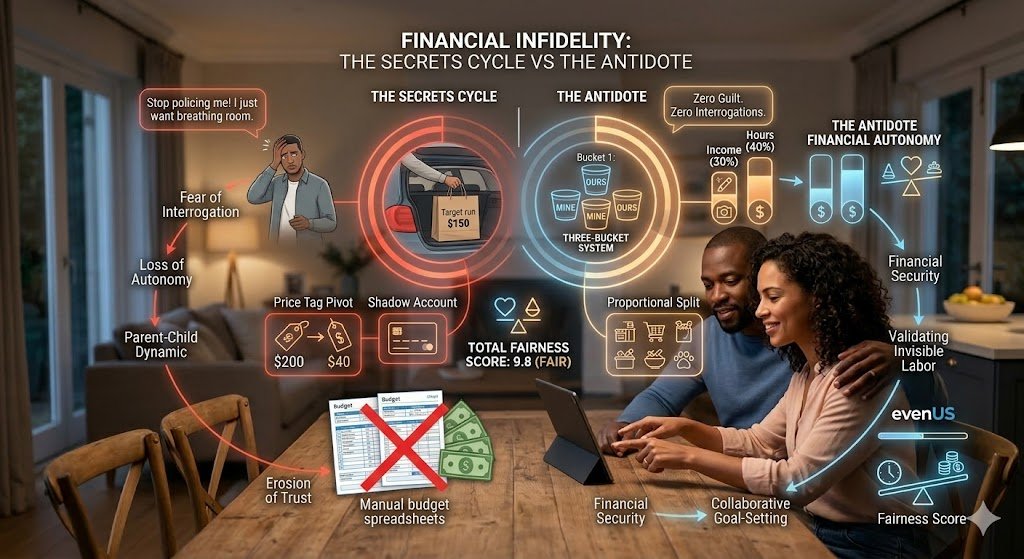

Stage 1: The “Price Tag Pivot” (The White Lie)

This is the entry-level tier of financial deception, and almost everyone has been guilty of it at some point. You aren’t hiding the physical item you bought, but you are intentionally manipulating the data to avoid a lecture.

- The Scenario: You buy a beautiful new jacket for $200. When you wear it for the first time, your partner notices and asks, “Oh, is that new? How much was it?” * The Pivot: Knowing your partner might think $200 is too steep, your brain makes a split-second calculation, and you reply, “Oh, this? I found it on the clearance rack for like $45.”

You tell yourself it’s just a white lie to avoid an unnecessary argument. But the danger of the Price Tag Pivot is that it slowly warps your partner’s understanding of the household cash flow. If $155 is “missing” from the joint account, the math stops making sense, leading to confusion and eventually, suspicion.

Stage 2: The “Trunk Stash” (The Crime of Omission)

The Trunk Stash occurs when the fear of judgment is so high that you start physically hiding the evidence of your spending. You aren’t just lying about the price; you are hiding the existence of the purchase entirely.

- The Scenario: You make a pit stop at Target after work and spend $150 on home decor, a new video game, or hobby supplies. As you pull into the driveway, you realize you don’t want to answer the inevitable question: “Did you really need to buy all that?”

- The Stash: Instead of walking through the front door with your bags, you leave them in the trunk of your car. Over the next week, you slowly sneak the items into the house one by one—maybe while your partner is in the shower or out running errands—so they blend into the background unnoticed.

When you start hiding shopping bags in your own home, you have officially shifted the relationship dynamic. You are no longer treating your partner like a teammate; you are treating them like a strict parent or a parole officer that you have to sneak around.

Stage 3: The “Shadow Account” (The Systemic Secret)

This is where the behavior escalates from a minor coping mechanism into a systemic breach of trust. A Shadow Account happens when one partner actively builds a financial wall to keep their spending entirely off the grid.

- The Scenario: You are tired of feeling guilty every time your partner reviews the shared credit card statement. To reclaim your freedom, you open a brand new credit card solely in your name.

- The Shadow: You select “paperless billing” and route the statements to a secondary, private email address. You use this card to fund hobbies, lunches out, or personal shopping, completely hidden from the family ledger.

This stage is incredibly dangerous because it allows debt to accumulate in the dark. If the “Us” entity (the couple) ever needs to apply for a mortgage, a car loan, or suddenly faces an emergency, that hidden debt will eventually be exposed, destroying the foundation of trust the relationship relies on.

The Psychology: Why Do We Hide the Receipts?

When a partner is caught hiding a purchase or lying about a price tag, the immediate reaction is usually anger and a demand for a character explanation: “How could you be so dishonest?” But if you want to fix the problem, you have to look past the lie and examine the environment that created it. Couples rarely lie about money out of malice or a desire to ruin the family finances. They lie out of self-preservation. When you dig into the psychology of a hidden receipt or a trunk stash, you almost always find a fundamentally broken communication system.

Here are the three psychological triggers that turn honest partners into financial hiders:

The Fear of the “Input Interrogation”

Imagine coming home after a long, stressful day at work. You bought a $6 coffee and a $20 book on your lunch break as a small treat to get you through the afternoon. The moment you walk in the door, your partner has the banking app open: “Did you really need to spend $26 today? We have coffee at home.”

This is the Input Interrogation. If every time you make a minor, everyday purchase your partner cross-examines you, you quickly learn a painful lesson: honesty leads to conflict.

To avoid the exhaustion of defending your daily choices, your brain naturally seeks the path of least resistance. You start using cash, or you downplay the cost, or you simply hide the bags. The financial lie isn’t about the money; it becomes a psychological defense mechanism against being constantly micromanaged.

The Loss of Autonomy

Adults have a fundamental psychological need for autonomy—the feeling that they are in control of their own choices. When you get married or move in together and merge your finances completely into one giant “Ours” pot without establishing clear boundaries, that autonomy vanishes.

Suddenly, every single purchase feels like a joint committee decision. You feel like you have to justify buying a video game, a new pair of running shoes, or a round of drinks for your friends.

Hiding money or making secret purchases is often a misguided, desperate attempt to reclaim a sense of individual freedom. The partner who hides a new golf club or a designer purse is usually silently screaming, “I work hard for a living, and I just want to buy something for myself without having to ask for permission!”

The Toxic “Parent-Child” Dynamic

When one partner acts as the household CFO—policing the budget, checking the statements, and scolding the other for overspending—the relationship deteriorates into a toxic Parent-Child dynamic.

- The “Parent” Partner: Feels burdened by the mental load. They feel like they are the only responsible adult in the house, constantly trying to keep the family ship afloat while their partner acts recklessly. They become resentful and controlling.

- The “Child” Partner: Feels scrutinized, lectured, and suffocated. Instead of stepping up to collaborate, they regress. They start acting like a rebellious teenager hiding things from a strict parent.

Nothing kills romance, intimacy, and trust faster than this dynamic. You cannot be romantic partners if one of you is handing out an allowance and the other is hiding their report card.

The Real Casualty is Trust, Not Cash

When the inevitable happens—when the hidden credit card bill arrives in the mail, or the partner accidentally opens the trunk to find bags of hidden purchases—the confrontation that follows is rarely about the math.

If you discover your partner secretly racked up $800 on a hidden account, you aren’t just angry about the $800. You might even have the cash in savings to pay it off immediately. The intense emotional reaction stems from something much deeper than the budget.

You are angry about the reality distortion.

The Shattering of Shared Reality

At its core, trust is the fundamental belief that your partner’s words match reality. When you build a life with someone, you operate under the assumption that you are both looking at the same map, facing the same financial facts, and working toward the same goals.

When you discover a hidden financial habit—even a relatively small one like the “Price Tag Pivot” or a “Trunk Stash”—that shared map catches fire. The immediate, painful thought isn’t, “How do we pay this off?” The immediate thought is, “If they looked me in the eye and lied to me about this for six months, what else are they lying about?”

The Ripple Effect of Doubt

Financial infidelity acts like a virus, infecting areas of the relationship that have nothing to do with money. This is the ripple effect of doubt:

- Questioning Past Conversations: You start replaying old conversations. “When they said they couldn’t afford to go to my sister’s wedding, was that true, or were they covering up this secret debt?”

- Assuming the Worst: If a partner lied about a $100 Target run, it is human nature to suddenly wonder if they are lying about where they go after work, who they are texting, or if they really paid the electric bill on time.

- The Exhaustion of Verification: The betrayed partner stops taking things at face value. They feel forced to become a private investigator in their own home, double-checking receipts, logging into bank accounts daily, and monitoring the mail.

From Teammate to Unpredictable Variable

A healthy relationship functions as a safe harbor. You face the unpredictability of the outside world—job stress, health scares, economic shifts—knowing that your partner is your reliable anchor.

Financial infidelity breaches that safety. It turns the person who is supposed to be your teammate into an unpredictable variable. You can no longer plan for the future—buying a house, having a child, or saving for retirement—because you no longer know if the financial foundation you are standing on is real or an illusion.

Once that safety is gone, the relationship is in critical danger. Healing doesn’t require a better budget; it requires entirely rebuilding the architecture of trust.

The Antidote: Guilt-Free “Mine” Money

When trust is broken by financial infidelity, the instinctive reaction of the betrayed partner is to tighten the leash. They demand passwords, set up daily transaction alerts, and insist on reviewing every single receipt.

But you cannot cure financial infidelity by demanding more transparency or tighter control. Tighter control doesn’t create honest partners; it just creates better liars.

The only permanent way to stop the secrecy is to remove the need for secrecy entirely. You do this by tearing down the monolithic “Ours” budget and transitioning to the Yours, Mine, and Ours method.

The Three-Bucket System

If you want to end the Parent-Child dynamic and restore autonomy to your relationship, you need to structure your bank accounts to reflect both your shared goals and your individual identities.

- Bucket 1: The “Ours” Account (The Household Engine) This account is strictly for shared, non-negotiable living expenses. Rent, utilities, groceries, shared streaming services, and date nights live here. Both partners contribute a fair, agreed-upon amount to this account every month to cover the collective overhead. Once the money is in this bucket, it belongs to the relationship, not the individual.

- Buckets 2 & 3: The “Mine” Accounts (The Autonomy Zones) Once your fair share of the “Ours” bills are paid, and your shared savings goals are met, whatever money is left over in your personal paycheck belongs entirely to you. This is your “Mine” money, and it lives in an account your partner does not manage.

The Golden Rule of “Mine” Money

Setting up the accounts is the easy part. The magic of this system relies entirely on enforcing one uncompromising boundary: The Golden Rule of “Mine” Money.

You cannot police, critique, comment on, or complain about how your partner spends their “Mine” money.

If your partner has paid their share of the rent and put money into the joint savings, their financial obligation to the household is complete. If they want to spend their remaining $200 on rare houseplants, an overpriced round of golf, or a collector’s item you think is ridiculous, they can do it with zero guilt and zero interrogations.

Why This Kills the “Trunk Stash”

When you establish an impenetrable perimeter of financial autonomy, the lying stops immediately.

There is absolutely no reason to hide a shopping bag in the trunk of your car if your partner has already agreed that the money used to buy it was yours to spend. The fear of the “Input Interrogation” vanishes. You no longer have to manipulate price tags or open shadow accounts because the system itself grants you the freedom you were previously trying to steal.

By giving each other permission to spend without judgment, you paradoxically build a much stronger foundation of trust.

Automate Honesty with EvenUS

Understanding the psychology of financial infidelity is the first step. Agreeing to the “Yours, Mine, and Ours” system is the second. But the third step—actually executing this system day after day—is where most couples stumble.

Transitioning to a new financial structure requires figuring out exactly what your fair contribution to the “Ours” bucket should be. If you try to calculate this manually on a spreadsheet, you inevitably bring the tension right back to the surface. You end up arguing over the math, debating who paid for what last week, and accidentally slipping back into the toxic Parent-Child dynamic.

You need a system that removes the friction, does the math for you, and acts as a neutral third party. That is exactly why we built EvenUS.

The “Anti-Spreadsheet” for Modern Couples

EvenUS is not just a budget tracker; it is a relationship operating system designed to automate transparency and enforce financial boundaries. Here is how it helps you stop keeping secrets and start building trust:

- Find Your Exact “Ours” Contribution: You don’t have to guess what is fair. Input your respective incomes, and EvenUS automatically calculates your exact Proportional Split for the shared household expenses. Once your fair share is covered, the system clearly delineates your remaining funds as your guilt-free “Mine” money.

- Validate the Invisible Labor: Financial contributions are only half the story of a relationship. EvenUS tracks your household “Zones” and daily chores. If you take on the mental load of managing the groceries or scheduling appointments, that invisible cognitive labor is finally made visible and validated.

- The Total Fairness Score: This is the ultimate antidote to financial suspicion. Our dashboard gives you a holistic look at your total contribution—combining your financial input with your time and effort to generate a Fairness Score.

Stop Policing and Start Partnering

When the system is objectively fair and managed by a neutral app, the resentment evaporates. The “Parent” partner no longer has to police the budget, and the “Child” partner no longer feels the need to hide a shopping bag in the trunk.

There is no need to rebel, hide, or lie when you are operating in a system that guarantees your autonomy while protecting the team.

Stop interrogating your partner over a $6 coffee and start protecting your relationship.

Download EvenUS today and build a system based on true equity and total transparency.

The Benchmark Study on Financial Infidelity Prevalence

Source: National Endowment for Financial Education (NEFE) Title: Financial Infidelity Polling (2021/2024) Why it supports your article: NEFE conducts the gold-standard national polls on this exact topic. Their research validates your “Spectrum of Infidelity” section, noting that nearly 2 in 5 Americans admit to committing financial infidelity, with hiding purchases and lying about prices being the most common infractions. It completely normalizes the behavior you are writing about. https://www.nefe.org/research/polls/2021/financial-infidelity-2021.aspx