Money is notoriously cited as the leading cause of stress and divorce in relationships. But here is the secret most financial advisors won’t tell you: Couples rarely fight about actual dollars and cents. When a conversation about a $50 takeout order spirals into a screaming match, you aren’t arguing about the food. You are arguing about what the money represents: control, safety, respect, and unseen labor.

If you want to merge your lives without tearing your relationship apart, you have to fundamentally change how you communicate about cash. Here is the blueprint for talking about money without the defensive walls coming up.

Talk about money without fighting

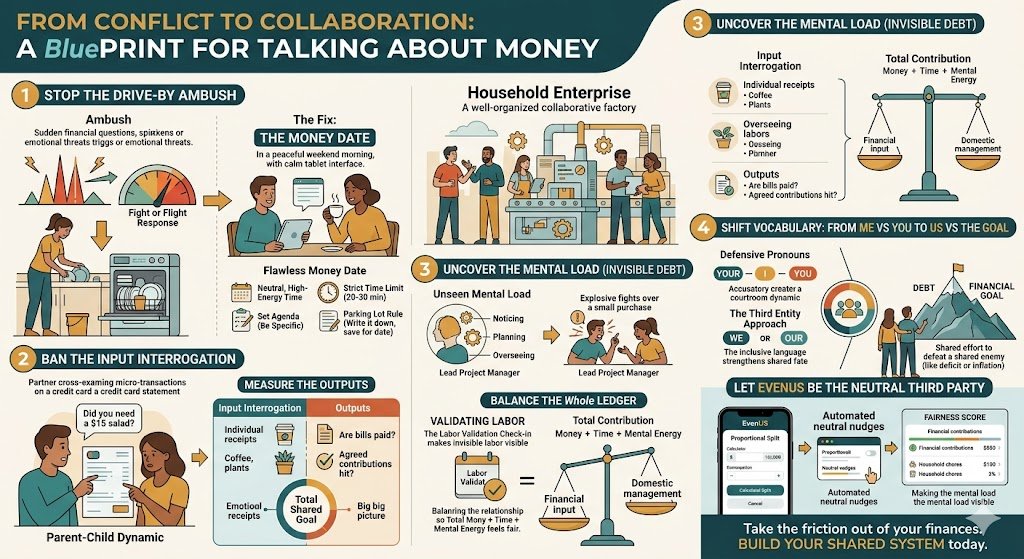

Stop the “Drive-By” Money Ambush

Think about the last time you and your partner fought about money. Chances are, it didn’t start at a kitchen table with a spreadsheet open. It probably started in the middle of a random Tuesday evening.

Maybe you were checking your banking app in line at the grocery store, noticed a charge you didn’t recognize, and the moment you walked through the front door, you blurted out, “Did you really spend $150 at Target today?”

This is called a “Drive-By Money Ambush,” and it is the single most destructive communication habit couples have regarding their finances.

The Psychology of the Ambush

When you drop a stressful financial question on your partner while they are unloading the dishwasher, wrangling the kids, or exhausted from a ten-hour workday, their brain does not register it as a simple math question. Their brain registers it as a threat.

In a fraction of a second, cortisol spikes and their “fight or flight” response is activated. They immediately feel criticized and micromanaged. Once that defensive wall comes up, rational problem-solving is entirely off the table. You are no longer two partners discussing a budget; you are two adversaries in combat.

The Fix: Treat Your Household Like an Enterprise

If you co-owned a small business, you would never corner your business partner in the hallway to aggressively question them about a budget deficit. You would schedule a meeting, pull the reports, and tackle the problem together.

You must treat your household with the exact same level of professional respect. You do this by establishing the “Money Date.”

How to Execute a Flawless Money Date

A Money Date is a scheduled, predictable time to review your shared financial engine. By putting it on the calendar, you completely remove the element of surprise, which instantly lowers the emotional temperature of the room.

Here are the four rules for a successful Money Date:

- Rule 1: Pick a Neutral, High-Energy Time. Never try to talk about money on a Sunday night at 10:00 PM when the “Sunday Scaries” are peaking. Pick a time when you are both relaxed and fed. Saturday morning over coffee or Thursday evening with a glass of wine or your favorite takeout works best. Make the environment inherently positive.

- Rule 2: Set a Strict Time Limit. A Money Date should not be a three-hour grueling marathon. Cap it at 20 to 30 minutes. If you know the conversation has a hard stop, it feels significantly less daunting to begin.

- Rule 3: Set an Agenda. Don’t just sit down and say, “Let’s talk about money.” That is too broad and anxiety-inducing. Be specific. “Hey, during our coffee date on Saturday, let’s take 20 minutes to figure out how we are funding the shared summer vacation.” * Rule 4: The “Parking Lot” Rule. If you get a sudden spike of financial anxiety on a Tuesday, do not ambush your partner. Write the thought down in a note on your phone (the “Parking Lot”) and save it for the scheduled Money Date on Saturday.

The Psychological Win: When both partners know exactly when the financial conversation is going to happen, the daily dread disappears. Your partner knows you aren’t going to randomly critique their spending on a Wednesday night, which allows them to actually relax in their own home. Anticipation replaces anxiety, and the defensive shields finally stay down.

Ban the “Input” Interrogation

Once you have successfully scheduled a Money Date and the defensive walls are lowered, you have to be incredibly careful about the language you use when reviewing the budget.

The quickest way to ruin a productive financial check-in is to fall into the trap of the “Input Interrogation.”

What is an Input Interrogation?

An Input Interrogation happens when one partner meticulously reviews the credit card statement and begins questioning the other’s daily, individual choices:

- “Did you really need to buy another plant for the living room?”

- “Why did you spend $18 on a salad for lunch today when we have food in the fridge?”

- “You bought another video game? Don’t you have three you haven’t played?”

These are questions focused entirely on the “inputs”—the micro-transactions required to get through a normal week.

The Psychology: The Parent-Child Dynamic

When you question a $15 lunch or a $40 hobby purchase, you probably think you are just trying to balance a spreadsheet. But to your partner, you are questioning their judgment, their maturity, and their right to enjoy their own hard-earned money.

Input interrogations immediately strip your partner of their adult autonomy. It shifts the relationship from a partnership of equals into a toxic Parent-Child dynamic. The questioning partner becomes the strict, scolding parent, and the questioned partner becomes the rebellious teenager who has to justify their allowance. Nothing kills romance and trust faster than this dynamic.

The Fix: Measure the “Outputs”

To stop fighting about money, you have to completely stop micromanaging the inputs and start measuring the “Outputs.”

The outputs are the macro-results of your shared financial engine. During your Money Date, instead of pulling up the line-by-line credit card statement to look for “mistakes,” you only need to answer two questions:

- Are the household bills paid in full?

- Did we both hit our agreed-upon proportional contributions to the shared savings goal this month?

If the answers to those two questions are “yes,” then the financial system is working perfectly.

Scripts for the Money Date

By focusing on the outputs, you shift the conversation from criticism to collaboration. Here is how to rephrase your concerns during a check-in:

- Instead of asking: “Why did you spend $100 on clothes this week?”

- Ask this: “It looks like the joint checking account is a little low before the electricity bill hits. Are we both still able to hit our proportional targets this month, or do we need to shift some funds around?”

- Instead of asking: “You spent way too much going out with your friends.”

- Ask this: “I really want to make sure we hit our $500 savings goal for the anniversary trip. Since we both had some fun weekends lately, how can we hack our budget this week to make sure we don’t fall behind on the trip fund?”

When you focus on the shared goal (the Output) rather than the individual purchase (the Input), you are treating your partner with respect. If the shared obligations are met, let the daily inputs go.

3. Uncover the “Invisible” Debt: The Mental Load

If you’ve ever had a massive, screaming match over a $15 pizza delivery or a $50 Target run, you know intuitively that the fight wasn’t actually about the money. In those moments, the bank statement is just a smokescreen for a much deeper, more painful issue: The Mental Load.

In many relationships, one partner acts as the “Lead Project Manager” for the household. They are the ones noticing that the milk is low, researching the best pediatrician, tracking the school calendar, and remembering that the dog needs a heartworm pill on the 15th. This is Cognitive Labor, and it is exhausting.

Why the Mental Load Triggers Money Fights

When one partner is carrying 80% of the household’s mental load, they are operating in a state of chronic “decision fatigue.” They feel like they are doing all the “heavy lifting” to keep the family ship afloat.

Now, imagine that “Project Manager” partner sees the other partner (who perhaps does very little of the planning) spend $200 on a new hobby or a night out without a second thought.

The result is an explosion. The partner who carries the mental load doesn’t see a $200 purchase; they see a partner who has enough free headspace to think about hobbies while they are drowning in domestic logistics. The “debt” being argued about isn’t financial—it’s a Labor Debt.

The Fix: Balance the Whole Ledger

You cannot have a peaceful, fair conversation about financial equity if you are ignoring labor equity. If you want to stop fighting about the credit card bill, you have to start acknowledging the invisible work happening behind the scenes.

The Strategy: The “Labor Validation” Check-in Before you dive into the numbers during your Money Date, start with a “Labor Check-in.”

- The Higher Earner/Lower Labor Partner should say: “I’ve noticed you’ve been carrying a lot of the logistics for the house and the kids lately. I want you to know I see that effort, and I don’t take it for granted. Before we look at the budget, is there anything on your plate that’s making you feel stressed or unsupported?”

- Why it works: Validating the invisible labor instantly diffuses financial tension. When a partner feels seen and appreciated for their cognitive work, they are significantly less likely to “nitpick” the other person’s spending. It shifts the dynamic from “You’re spending our money while I do all the work” to “We are both contributing to this household in different, valuable ways.”

Making the Invisible Visible

The goal is to move toward a relationship where the Total Contribution—money + time + mental energy—feels balanced. If one partner provides more of the financial “input,” the other may provide more of the domestic “management.” As long as both partners agree the trade-off is fair, the resentment disappears.

Shift the Vocabulary: From “Me vs. You” to “Us vs. The Goal”

Language is the steering wheel of a conversation. Even with the best intentions, using the wrong pronouns can accidentally trigger a “defensive crouch” in your partner. When we are stressed about money, we naturally tend to use isolating, accusatory language:

- “Your credit card bill is getting out of control.”

- “I am the one paying for everything while you just spend.”

- “You need to stop buying so much takeout.”

This language creates a courtroom dynamic. You are the prosecutor, and your partner is the defendant. In this scenario, nobody wins.

The Strategy: The “Third Entity” Approach

To stop fighting, you must stop treating your partner as the problem. Instead, you must treat the financial challenge as a “Third Entity”—an external obstacle that you are both teaming up to defeat.

By shifting the vocabulary, you move from being adversaries to being co-CEOs of your household. You aren’t fighting each other; you are fighting the deficit, the debt, or the inflation.

The Script Shift: Pronoun Reframing

Here is how to practically reframe your most common financial stressors:

- Instead of: “Your spending is the reason we can’t save for a house.”

- Try: “Our house-deposit fund is growing slower than we planned. What can we do together this month to protect that goal?”

- Instead of: “I’m tired of being the only one who cares about the budget.”

- Try: “I’m starting to feel some anxiety about our shared overhead. Can we look at the numbers together this weekend so I don’t feel like I’m carrying the financial planning alone?”

- Instead of: “You spent $200 on that hobby again.”

- Try: “I noticed a $200 dip in our projected buffer. Does that change our plan for the upcoming utility bills, or are we still in the clear?”

The Power of “We”

Using “We” and “Our” isn’t just about being polite; it’s about reinforcing the shared fate of the relationship. When you use inclusive language, you remind your partner that their success is your success, and their struggle is your struggle. This creates a safe emotional environment where your partner feels comfortable admitting a mistake or a spending slip-up without fearing a lecture.

Let EvenUS Be the “Neutral Third Party”

The ultimate hack for ending money fights is to remove yourselves from the administrative friction entirely. You need a system that acts as the neutral manager, so you and your partner can just go back to being partners.

That is exactly why we built EvenUS.

EvenUS removes the emotion from the math and the nagging from the relationship:

- No More Math Arguments: Input your incomes and expenses, and EvenUS automatically calculates your fair, Proportional Split. The app tells you what is fair, so you don’t have to debate it.

- Automated Neutral Nudges: Stop nagging your partner to pay their half of the bill or take out the trash. Let the app send the notification.

- Validate the Mental Load: The EvenUS dashboard tracks both financial contributions and household chores, generating a holistic Fairness Score. You can finally see—and validate—everything your partner does behind the scenes.

When the system is fair and the invisible labor is visible, the fights stop.

Take the friction out of your finances. Download EvenUS and start your first stress-free Money Date today.

Language and Conflict Resolution

Title: The Seven Principles for Making Marriage Work (Financial Chapter) Author: Dr. John Gottman (The Gottman Institute) Why it supports your article: Dr. Gottman is the world’s leading researcher on relationship stability. His “Softened Start-up” technique is the direct inspiration for the Section 4 strategy of moving from “Me vs. You” to “Us vs. The Goal.” Linking to the Gottman Institute adds immense psychological authority to your communication tips.

- Credible Link: https://www.gottman.com/blog/manage-conflict-the-six-skills/