Manage Household Finances Without a Joint Bank Account

For many modern couples, the traditional “merger” of bank accounts feels like a relic of a different era. Whether you are entering a partnership later in life with established assets, prioritizing individual financial agency, or simply preferring the interface of your existing banking app, the decision to maintain separate accounts is increasingly common. In fact, recent consumer banking trends show a significant rise in “financial autonomy,” particularly among Millennial and Gen Z couples who value independence alongside partnership.

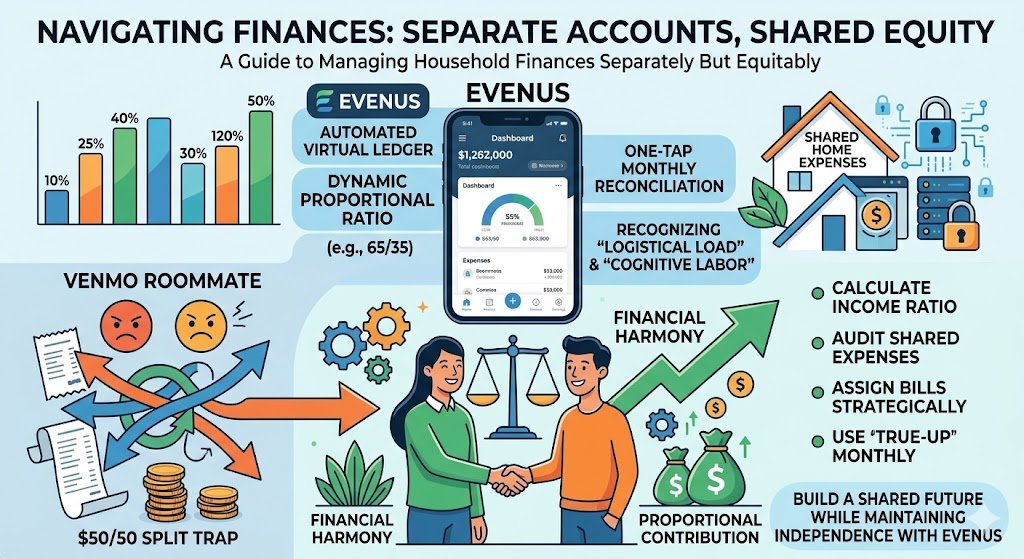

However, choosing to forgo a joint bank account does not exempt a couple from the complexities of household management. When the mortgage is due, the grocery fridge is empty, and the utility bills land in the inbox, a system is required. Without a clear framework, couples with separate accounts often slide into the “Venmo Roommate” trap—a cycle of constant nickel-and-diming, tedious receipt tracking, and simmering resentment over who paid for the last three sushi dinners.

The good news is that you can maintain 100% separate accounts and still achieve a state of perfect financial harmony. By moving away from manual spreadsheets and embracing a “Virtual Ledger” mindset, you can build a system of true equity without ever stepping foot in a bank to open a joint account.

Here is the definitive guide to managing household finances separately but equitably.

1. The Psychological Trap of the “50/50 Separate Split”

The most common mistake couples make when keeping accounts separate is defaulting to a rigid 50/50 split of all shared costs. On the surface, this feels like the ultimate form of “fairness”—each person pays half.

However, as sociological research in the Journal of Marriage and Family suggests, 50/50 splits in the presence of unequal earnings actually create a systemic power imbalance. If Partner A earns $90,000 and Partner B earns $45,000, a $2,000 monthly rent bill represents a minor line item for the higher earner but a massive, suffocating percentage of the lower earner’s take-home pay.

When accounts are separate, this disparity is often “hidden.” The higher earner sees their personal savings grow rapidly, while the lower earner’s account remains perpetually near zero. This leads to Financial Siloing, where one partner feels like a wealthy benefactor and the other feels like a struggling dependent. To avoid this, couples must replace the “Equal Dollar” mindset with a “Proportional Contribution” mindset.

2. Framework 1: The “Assigned Bills” Method (The Hands-Off Approach)

If you want to minimize the number of transfers between your separate accounts, the Assigned Bills method is the most efficient. Instead of pooling money into a shared pot, you divide the actual bills themselves based on your Income-Proportional Ratio.

How to Execute:

- Calculate the Ratio: Add your two net incomes together. Determine what percentage each person contributes to the total. (e.g., Partner A provides 65%, Partner B provides 35%).

- Audit the Shared Expenses: List every recurring household cost: rent/mortgage, insurance, utilities, internet, streaming services, and a monthly grocery estimate.

- Assign the Ownership: Partner A takes the “big” bills (like the mortgage), while Partner B takes a cluster of “smaller” bills (utilities + groceries + car insurance).

- Balance the Totals: The goal is for the total dollar amount of bills in Partner A’s name to equal roughly 65% of the total household cost, and Partner B’s to equal 35%.

The Benefit: Once set up, this system is “set and forget.” You each pay your assigned bills from your own accounts, and the math remains fair without needing a joint account or monthly “settling up.”

3. Framework 2: The “Virtual Ledger” (Monthly Reconciliation)

For couples whose expenses fluctuate wildly—perhaps due to frequent dining out, travel, or variable grocery costs—the Assigned Bills method can feel too restrictive. In these cases, a Monthly Reconciliation (or “True-Up”) is more effective.

In this model, you both pay for things as they come up throughout the month. One person might grab the groceries on Tuesday; the other pays for the flight tickets on Friday. You keep your separate accounts, but you track every shared expense in a central location.

The Mathematics of the True-Up:

At the end of the month, you tally the total shared spending. If you’ve agreed on a 60/40 split:

- Total Shared Spend: $4,000.

- Partner A’s Required Contribution (60%): $2,400.

- Partner B’s Required Contribution (40%): $1,600.

- The Adjustment: If Partner A actually paid $3,000 during the month and Partner B only paid $1,000, then Partner B simply sends one lump-sum transfer of $600 to Partner A to balance the ledger.

The Benefit: This allows for maximum flexibility and ensures that every dollar spent on the “Us” entity is accounted for proportionally.

4. The Critical Component: Accounting for the “Logistical Load”

When couples manage finances through separate accounts, the Mental Load of household administration often goes unnoticed. Even if the money is split 60/40, the physical act of paying the bills—logging into five different utility portals, tracking the property tax deadlines, and auditing the grocery receipts—usually falls on one person.

Research published in the American Sociological Review highlights that this “Cognitive Labor” is a distinct form of work that is just as exhausting as physical labor or financial contribution.

If you are the partner who manages the separate accounts, handles the “True-Up” math, and ensures the rent is sent on time, you are contributing significantly more than just your share of the money. A truly equitable system must validate this. In a “Virtual Ledger” model, the partner handling the logistics should have their effort explicitly recognized—perhaps by adjusting the financial ratio slightly or ensuring the other partner takes on an equivalent “Zone” of household management (like meal planning or pet care).

5. Why Spreadsheets Fail Independent Couples

Most couples who choose to keep accounts separate attempt to manage the “Virtual Ledger” using a shared spreadsheet or a notes app. This is where the system usually collapses.

Manual tracking requires a level of administrative discipline that few people can maintain long-term. Receipts get lost, one person forgets to log a dinner, and the end-of-month “reconciliation” turns into an interrogation: “Wait, what was this $84 charge on the 12th?” This friction creates the exact type of money-related conflict you were trying to avoid by staying separate.

To make separate-account management sustainable, you need an automated, neutral third party.

6. Automate Your Virtual Equity with EvenUS

The EvenUS app was built specifically for the modern couple who wants to be “Separately Combined.” It provides the benefits of a joint account (visibility and shared math) without the drawbacks (loss of privacy and bank paperwork).

- The Virtual Joint Ledger: EvenUS acts as your shared financial brain. You don’t need to open a new bank account. You simply link your separate accounts, and the app tracks your “Shared” spending automatically.

- Dynamic Proportional Math: EvenUS calculates your exact income-proportional ratio in real-time. If one partner gets a raise or a bonus, the “fair share” updates instantly. No more manual calculations.

- One-Tap Reconciliation: At the end of the month, EvenUS tells you exactly who owes what to maintain your fairness goals. You can “settle up” with a single click, eliminating the “Venmo Roommate” arguments forever.

- Track the Logistical Load: EvenUS is the only app that allows you to log domestic work and household management alongside your finances. If you’re the one paying the bills, the app factors that effort into your Total Fairness Score.

Keeping your bank accounts separate is a powerful way to protect your individual identity and financial autonomy. By utilizing a “Virtual Ledger” system and automating the math with EvenUS, you can ensure that your separate paths are always leading toward a shared, equitable future.

To validate the “Proportional Split” (Section 1)

Source: Journal of Marriage and Family Study: Pool It or Pool It Not? Impact of Financial Management on Marital Satisfaction (2022) Authors: Dr. Joanna Pepin, et al. Why it fits your article: This study explores how different financial management styles affect relationship quality. It specifically highlights that while separate accounts can maintain autonomy, they often lead to “financial siloing” and lower satisfaction if not managed with a clear, equitable system like the proportional model.

- Expert Link: https://onlinelibrary.wiley.com/journal/17413737