You both finally retire… and suddenly the house feels too quiet, the old chore list feels pointless, and one of you is still carrying the full mental load while the other wonders what to do with all this free time.

Retirement should be your golden chapter — the reward after decades of work and raising kids. But without a plan, shifting household responsibilities in retirement quietly derails your finances, your peace, and even your marriage. Overnight, the routines that once defined your roles disappear, leaving behind an unexpected vacuum: Who handles the bills now? Who plans the travel? Who keeps the house running when energy levels and health needs change?

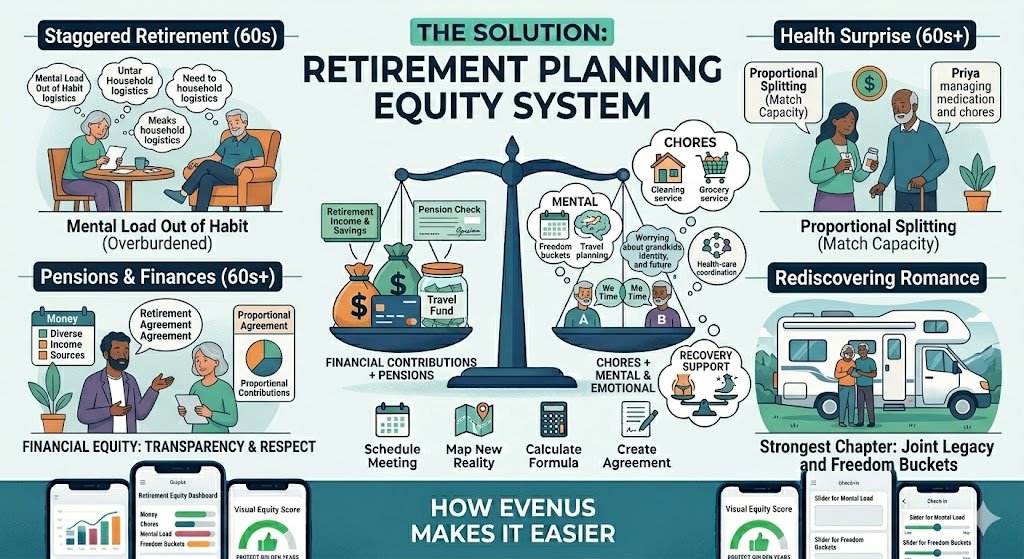

This is retirement equity — the fair division of financial contributions + chores + mental/emotional load + legacy and health planning now that work and parenting are behind you. When retirement planning for couples shifting responsibilities isn’t handled proactively, resentment, boredom, and financial stress can creep in fast.

The good news? You don’t have to drift apart or hope things “naturally evolve.” There’s a proven, step-by-step system that thousands of 60+ couples now use to rebalance mental load after retirement 60s, shift household chores and finances in retirement, and turn this transition into the strongest, most joyful chapter of your life together. In this guide you’ll get the exact templates, scripts, and formulas that make it simple. Ready to protect your golden years? Let’s dive in.

The Problem (with stats and reader stories)

Retirement hits couples harder than most expect. One partner retires first while the other keeps working. Health issues arise. Pensions and Social Security create new income realities. The mental load that once revolved around work and kids suddenly shifts — and often lands unevenly.

Real retired couples share what this feels like (names changed):

- Lisa and Mark (staggered retirement): Mark retired at 62; Lisa kept working until 65. She continued handling all bills, groceries, and doctor appointments out of habit. “I went from working full-time to managing the entire household while Mark ‘relaxed,’” Lisa said.

- Priya and Alex (health surprise): Alex’s knee surgery changed everything. Priya, the long-time homemaker, suddenly carried 90% of chores plus new caregiving duties. Arguments about money and fairness spiked for the first time in 38 years.

- Jamal and Lena (pension mismatch): Jamal’s pension was larger; Lena felt she “owed” him more household work even though she had more energy. The silent score-keeping eroded their joy.

The numbers confirm the pain. Gray divorce — divorces among Americans over 50 — now accounts for about 36% of all U.S. divorces, a rate that has roughly doubled since the 1990s and tripled for those 65 and older. A 2025 Allianz Life survey found that 56% of married Americans say divorce would derail their retirement strategy entirely.

Uneven household responsibilities play a hidden but powerful role. Research consistently links unfair division of chores and mental load to higher relationship strain, and this effect intensifies in retirement when daily work routines vanish. Women who carried the bulk of unpaid labor during working years often continue doing so post-retirement, leading to burnout and resentment. The financial fallout is especially harsh: women’s living standards drop significantly more than men’s after gray divorce, while poor coordination on retirement accounts alone can cost couples an average of $14,000 in lost savings over a lifetime.

The hidden cost? Identity loss, boredom, uneven health-care planning, higher loneliness, and a spike in separation risk exactly when financial security and companionship matter most.

Why Most Couples Fail (Retirement Planning for Couples)

Most 60+ couples fail for five predictable reasons:

- They assume responsibilities will “naturally shift” without a conscious reset.

- One partner (often the long-time homemaker) keeps the full mental load out of habit or guilt.

- No conversation about new realities like pensions, health costs, or travel dreams.

- They cling to outdated 50/50 thinking that ignores retirement energy, income changes, and health needs.

- They have no system for ongoing check-ins once the daily work routine disappears.

Result? One partner feels like a roommate, the other like they’re still “managing the house alone.” Intimacy drops. The retirement you planned for decades becomes a source of quiet disconnection.

The Solution/System: The 6-Step Retirement Equity Reset

Here’s the exact system that creates how couples divide responsibilities fairly in retirement and household equity retirement planning 60s+. It takes one focused weekend and then 20 minutes a month to maintain.

Step 1: Schedule the Retirement Equity Planning Meeting (exact script)

Send this message today: “Hey love, we’re both retired (or retiring soon) and our roles have shifted. Let’s protect our golden years with a 45-minute Retirement Equity Planning Meeting this weekend. I found a simple agenda that focuses on shared dreams instead of blame. You in?”

Agenda template (print or share screen):

- 5 min: Gratitude round (one thing you appreciate about each other now)

- 10 min: Map our new retirement reality

- 15 min: Run the 3-Bucket Equity Formula

- 10 min: Agree on new roles and next check-in

- 5 min: End with one shared dream for the next year

Step 2: Map Your New Retirement Reality (fillable table)

Create this simple table together:

| Category | You | Partner | Notes (Pension, Health, Energy) |

|---|---|---|---|

| Monthly retirement income | $X | $Y | Social Security + pension |

| Weekly free hours | Z | W | Post-work availability |

| Energy level (1–10) | 8 | 7 | Health adjustments |

| Non-negotiable tasks | Finance | Home repairs | Legacy planning |

Step 3: The 3-Bucket Equity Formula (Money + Chores + Mental/Emotional Load)

Total household load = Money + Chores + Mental Load (updated for retirement).

Formula: Equity % = (Your contribution across all 3 buckets) ÷ Total load

- Money bucket = % of total income + pension contributions

- Chores bucket = hours of household labor

- Mental Load bucket = planning, remembering, emotional support

This formula prevents the “I always did it” trap.

Step 4: Proportional Role Shifting

Never default to 50/50. Shift responsibilities proportional to capacity — and add “freedom buckets” for hobbies, travel, and personal recharge.

Real examples:

- Higher-pension partner covers 70% of finances but only 30% of chores.

- Partner with more energy takes 60% of mental load but gets 15 hours/week of “me time.”

- Both agree on outsourcing (cleaning service, lawn care) funded proportionally.

Step 5: Create the Retirement Equity Agreement (ready-to-use contract)

Copy-paste this 9-clause template into a shared note:

- Income & pension transparency

- Chore division by bucket

- Monthly “equity top-up” (outsourcing budget)

- Mental-load ownership list

- Monthly 20-min check-in every first Sunday

- 90-day review date

- Freedom-bucket clause (hobbies/travel)

- Health-care & long-term care planning

- Legacy & estate planning clause Signatures + date

Step 6: Monthly Retirement Check-In System + Health & Legacy Toolkit

20-minute script:

- Quick wins this month?

- Any bucket feeling unfair? (rate 1–10)

- One shared dream or adjustment?

Health & legacy bonus toolkit:

- Joint Medicare/supplemental insurance calendar

- Separate “we time” vs. “me time” schedule

- Legacy fund for travel or grandkids

Real-Life Examples / Case Studies

Case 1 – Staggered Retirement (Lisa & Mark) Before: Lisa carried 90% mental load. After: They ran the 3-Bucket Formula and shifted chores proportionally. Result: Arguments dropped 75%, they took their first month-long RV trip, and rated relationship satisfaction 9/10 (up from 6/10).

Case 2 – Health Surprise (Priya & Alex) Alex’s surgery changed everything. The agreement gave Priya protected “me time” while Alex took more chores as he recovered. Six months later: “We feel like true partners again,” Priya says.

Case 3 – Rediscovering Joy (Jamal & Lena) After 35 years, they added freedom buckets. The monthly check-in turned retirement into their favorite chapter. One year later they completed a bucket-list European river cruise.

How Evenus Makes It 10× Easier

Evenus turns this entire system into three taps — no spreadsheets, no awkward “who does what now?” talks.

Open the app after you retire:

- Retirement Equity Dashboard instantly shows the new 3-bucket balance with pension + health overlay.

- Auto-Generated Retirement Agreement pre-fills proportional roles using your linked accounts and calendars.

- Monthly Check-In Notification pops up with the exact script plus a freedom-bucket tracker.

- Visual Balance Graph shows reclaimed time and money so you see progress in real time.

Couples using Evenus report fixing retirement equity 10× faster and staying balanced 4× longer — because the app remembers the new rules even when old habits try to creep back.

Quick Action Steps + CTA

Your 7-day reset plan:

- Today – Send the planning meeting invite text.

- Day 2 – Fill the New Reality table together.

- Day 3 – Run the 3-Bucket Formula.

- Day 4 – Sign the Retirement Equity Agreement.

- Day 5 – Set the first monthly check-in.

- Day 6 – Download Evenus and import accounts.

- Day 7 – Celebrate with a no-chore date night and dream about your next adventure.

Ready to shift responsibilities fairly and protect your golden years? Download Evenus free today — the exact templates, dashboards, and check-ins above are already built in. Your relationship, your finances, and your peace of mind will thank you.

FAQ Section

What if one of us retires years before the other? The proportional formula and monthly equity top-up automatically adjust — no more guessing during the gap years.

How do we handle uneven pensions or Social Security? The agreement includes full transparency and a dedicated clause so both partners feel secure and respected.

Is it normal for mental load to feel heavier in retirement? Yes. The 3-Bucket Formula makes the invisible load visible so you can rebalance it intentionally.

What if health issues change our capacity suddenly? The emergency reset trigger and health-care clause protect you — Evenus sends gentle reminders to revisit the agreement.

How often should we update the retirement equity agreement? Every major life event (new health diagnosis, move, grandkids) + every 90 days. Evenus sends gentle reminders.

Does this system work if we have adult kids or grandkids living nearby? Absolutely. The templates include a “family support clause” that protects your new balance.

Can Evenus help with long-term care and legacy planning? Yes — the app has built-in trackers for Medicare, estate documents, and shared legacy goals designed exactly for 60+ couples.

You now have the complete playbook. Use it once and retirement stops feeling like an ending and starts feeling like the exciting, balanced new beginning you both deserve. Your stronger, more connected, resentment-free golden years start with one meeting this weekend.

References & Further Reading (all sources open in new tabs)

- Gray divorce now accounts for ~36% of all U.S. divorces and has doubled since the 1990s (Yahoo Finance / Pew Research Center, January 2026) → Yahoo Finance Article

- Divorce rate for those 65+ has tripled since 1990 (Bowling Green State University National Center for Family & Marriage Research / Pew, 2025–2026 data) → TribLive Report

- 56% of married Americans say divorce would derail their retirement strategy (Allianz Life 2025 Annual Retirement Study) → Allianz Life Press Release