Practical Tips to Eliminate Money Related Conflicts in Marriage- Money has historically been cited as the number one source of friction, stress, and divorce in modern marriages. Yet, when couples find themselves arguing over a credit card bill, a fluctuating utility cost, or the price of a weekend getaway, the fight is almost never actually about the dollars and cents.

Financial conflicts in a relationship are almost entirely rooted in deeper, unaddressed issues of power, individual autonomy, and the desperate human need to feel valued.

When couples move in together or get married, they typically rely on deeply outdated societal advice—specifically, the mandate to either dump every single penny into one giant shared pot or to split every single expense rigidly down the middle. Both of these extremes accidentally create systems that breed silent resentment.

To permanently eliminate money-related arguments from your marriage, you must stop treating your relationship like a corporate merger or a collegiate roommate agreement. You need a system built on true equity, radical transparency, and mutual validation. Here are five practical, proven tips to revolutionize how you and your partner manage your shared financial life.

Practical Tips to Eliminate Money Related Conflicts in Marriage

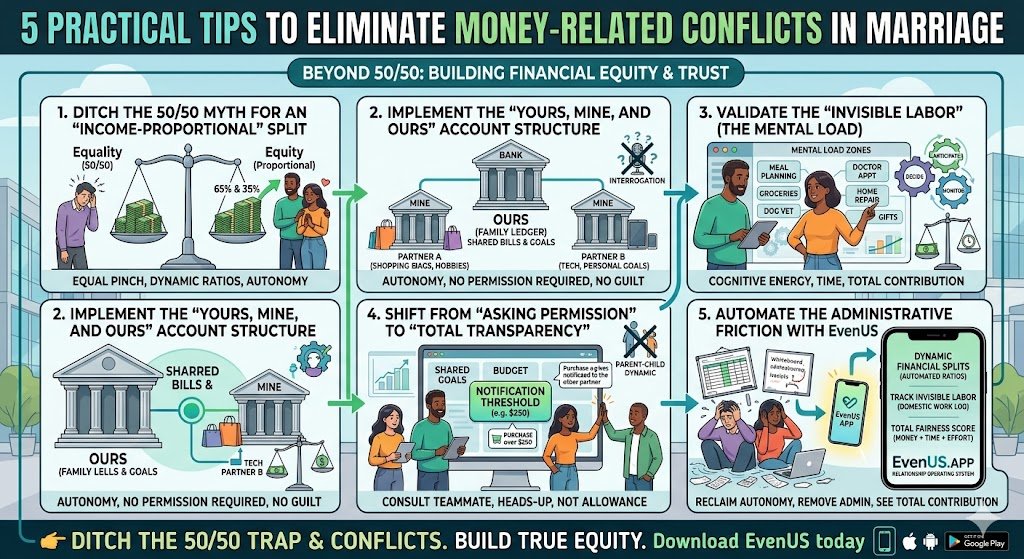

1. Ditch the 50/50 Myth for an “Income-Proportional” Split

The absolute quickest way to build silent resentment in a marriage is to force a 50/50 financial split when there is a significant gap in your respective incomes.

A 50/50 split feels clean and mathematically “fair” on paper, but it assumes both partners are experiencing the exact same economic reality. If Partner A earns $100,000 a year and Partner B earns $50,000 a year, forcing both of them to pay $2,000 a month for the mortgage creates immediate systemic inequality.

For the higher earner, that $2,000 is a manageable fraction of their take-home pay, leaving them with ample surplus cash to invest, save, or spend on hobbies. For the lower earner, that identical $2,000 bill consumes nearly half of their entire monthly income. This creates a state of Financial Suffocation. The lower earner is left scraping by, completely stripped of their financial autonomy.

The Practical Fix: The “Equal Pinch” You must transition away from equal dollars and move toward equal effort. This is achieved through an income-proportional split.

- Add your total monthly take-home pays together to find your “Total Household Income.”

- Calculate what percentage each partner contributes to that total. If you bring in 65% of the total household income, you are responsible for covering 65% of the shared household bills.

- If your partner brings in 35%, they cover 35% of the bills.

This framework ensures that both partners feel the exact same relative financial “pinch.” Most importantly, it leaves both individuals with a fair, proportional amount of discretionary cash that they can call their own.

2. Implement the “Yours, Mine, and Ours” Account Structure

If the 50/50 split is the first trap, pooling 100% of your money into a single joint checking account is the second.

When every single dollar you earn is dumped into a shared pot, every single purchase you make becomes subject to your partner’s judgment. This inevitably leads to what relationship psychologists call the “Input Interrogation.” You buy a coffee, and your partner asks why you didn’t just make it at home. You buy a new pair of shoes, and you feel a wave of guilt, perhaps even leaving the shopping bag in the trunk of your car to avoid a lecture. This loss of independence is a primary driver of financial infidelity.

The Practical Fix: The Three-Account Architecture To maintain a healthy marriage, you must balance the “Us” entity with the “I” entity. You do this by setting up a specific banking architecture:

- The “Ours” Account (The Family Ledger): Open one joint checking account. Every payday, both partners automatically transfer their proportional percentage (calculated in Tip 1) into this account. This ledger is strictly for shared household bills: rent, utilities, groceries, and joint savings goals.

- The “Mine” Accounts: Whatever money is left over from your paycheck after you have funded the Family Ledger stays in your individual, personal checking account.

The golden rule of the “Mine” account is total autonomy. This is your money. You have already paid your fair share to the household, so you can spend this remaining cash however you want, without needing permission, justifying the cost, or facing criticism from your partner.

3. Validate the “Invisible Labor” (The Mental Load)

A purely mathematical financial split, even a proportional one, will still feel deeply unfair if the partner who earns less money is simultaneously expected to manage 90% of the household logistics.

A marriage does not run on dollars alone. It runs on capital, physical time, and cognitive energy. Often, the partner with the slightly lower income or the more flexible job absorbs the Mental Load. This is the invisible, exhausting, behind-the-scenes work of running a shared life.

It is the labor of anticipating that the dog needs a vet appointment, researching the right clinic, making the decision on the schedule, and monitoring the calendar to ensure someone actually takes the dog. It is auditing the pantry, planning the meals, and remembering your in-laws’ birthdays.

The Practical Fix: Measure “Total Contribution” If you only track the money deposited into the bank account, the partner managing the mental load will eventually burn out from feeling unseen and undervalued. True equity requires you to factor household management into your relationship’s balance sheet. The time spent managing the grocery inventory or organizing the family schedule must be explicitly validated and treated as a massive, tangible contribution to the relationship’s overall equity.

4. Shift from “Asking Permission” to “Total Transparency”

Many marital arguments are sparked by a single, seemingly innocent phrase: “Is it okay if I buy…” For an adult who works hard for a living, having to ask a romantic partner for permission to make a purchase creates a deeply toxic Parent-Child dynamic. The higher earner becomes the gatekeeper of the lifestyle, acting as a parent handing out an allowance. The lower earner is reduced to a dependent. This dynamic kills romance, mutual respect, and adult agency.

The Practical Fix: The Notification Threshold If you have properly established your proportional split and your autonomous “Mine” accounts, you never have to ask permission to spend your own money.

However, for larger, shared purchases that come out of the joint Family Ledger (like a new couch or booking a flight), you should establish a “Transparency Threshold.” Sit down and agree on a dollar amount—for example, $250. Any shared purchase under $250 can be made at either partner’s discretion. Any shared purchase over $250 simply requires a heads-up conversation.

You are not asking for permission; you are consulting your teammate. It is a shift from seeking allowance to operating with total transparency and shared goals.

5. Automate the Administrative Friction with EvenUS

The theories of proportional splitting and validating the mental load are beautiful, relationship-saving concepts. However, the manual execution of these concepts is where most couples fail.

Couples often start with the best of intentions, building a shared Excel spreadsheet to track their proportional math and creating a whiteboard checklist for daily chores. But life is incredibly dynamic. Salaries change due to bonuses or lost hours, utility bills spike in the winter, and tracking who actually spent two hours meal-planning on a Sunday becomes a tedious, administrative nightmare. Eventually, the friction of maintaining the spreadsheet sparks its own arguments, the system is abandoned, and the couple defaults back to financial chaos.

The Practical Fix: The Relationship Operating System To make financial equity sustainable, you must remove the administrative friction. You need a neutral, automated third party, which is exactly why modern couples rely on the EvenUS app.

EvenUS is designed specifically to eliminate money-related conflicts by automating fairness:

- Dynamic Financial Splits: You simply input your incomes, and EvenUS automatically calculates your exact proportional split. If a salary changes or a bonus hits, the math updates instantly. There are no spreadsheets to maintain and no math to argue over.

- Tracking the Invisible Labor: EvenUS is the first platform to solve the “money-only” flaw. The app allows you to explicitly track household “Zones,” chore management, and the exhausting cognitive labor that keeps your life running. We make the invisible work highly visible.

- The Total Fairness Score: By combining your financial input with your time and domestic effort, the app generates a single, real-time Fairness Score.

When you have a clear, automated system that proves both partners are pulling their weight in their own unique ways, the anxiety of “who paid for what” completely disappears.

Stop letting outdated advice and spreadsheet friction dictate the health of your marriage. Reclaim your individual autonomy, validate your partner’s invisible labor, and build a unified future.

2. To validate the “Invisible Labor” (Tip #3)

Source: American Sociological Review Study: The Cognitive Dimension of Household Labor (2019) Author: Allison Daminger (Harvard University) Why it fits your article: This is the foundational sociological paper that defines and categorizes the “Mental Load.” It proves that cognitive labor (anticipating, identifying, deciding, and monitoring) is a distinct, exhausting form of work that disproportionately falls on one partner and is typically ignored in financial discussions.